The Great Reconstruction of the Global Auto Industry ( US vs. China Economy Part 2 )

Over the past five years, the global automotive market has undergone a profound "migration of power sources." As of 2026, this reconstruction has entered a fever pitch: the sales and market share of Electric Vehicles (EVs) continue to climb, while the living space for traditional Internal Combustion Engine (ICE) vehicles is being eroded at a rate of approximately 3% to 5% annually.

1. Tesla: The Spark That Ignited the Revolution

The explosion of the EV market is inseparable from Tesla’s role as the "icebreaker." Through its star products, the Model 3 and Model Y, Tesla not only validated the commercial viability of pure electric mobility but also held the top spot in global EV sales for a prolonged period.

- The Sales Legend: In 2021, Tesla delivered approximately 936,000 units worldwide, proving to the world for the first time that EVs could become mainstream. Although BYD surpassed Tesla in annual Battery Electric Vehicle (BEV) sales in 2025 (delivering approximately 2.26 million units), Tesla’s multi-year dominance from 2021 to 2024 provided the initial economies of scale that matured the global EV supply chain.

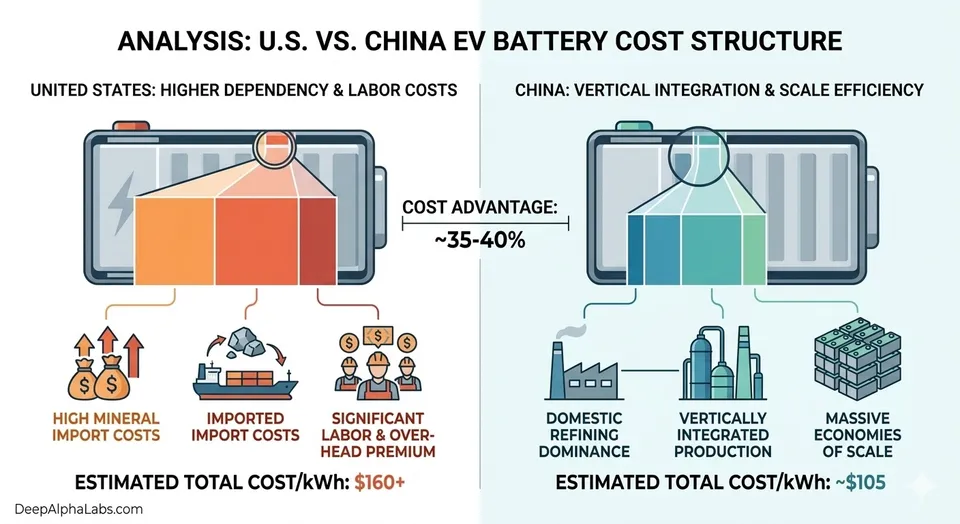

2. China: "Vertical Dominance" Across All Industrial Categories

If Tesla provided the spark, China has built the "Gigafactory" that covers the entire industrial chain. By 2026, China has demonstrated overwhelming advantages across all industrial categories:

- Whole-Chain Optimization: China does not just manufacture cars; it controls every "cell" of the vehicle.

- Minerals and Materials: China controls the processing of most of the world's lithium and cobalt, as well as the production of graphite anodes.

- Core Batteries: CATL and BYD together command over 50% of the global battery market.

- Operating Systems and Intelligence: Tech giants like Huawei, Xiaomi, and Baidu are deeply integrated into the automotive ecosystem, redefining the car from a "mechanical product" to an "electronic product."

- The World's Largest Exporter: In 2025, China's EV exports exceeded 1.3 million units. To bypass tariff barriers, Chinese automakers are shifting from "selling abroad" to "setting down roots":

- Case Studies: BYD is constructing plants in Hungary, Brazil, and Thailand; Chery is collaborating with local brands in Spain for production; and SAIC’s planned large-scale production base in Europe broke ground in early 2026.

3. The U.S. Auto Industry: "Crisis" and "Opportunity"

The U.S. automotive industry currently faces a "triple threat": high costs, slow transition, and policy volatility. Traditional Detroit giants (such as GM and Ford) are struggling under the weight of heavy pension burdens and the difficulty of repurposing legacy production capacity.

Can EVs be the solution? The answer is yes, but only if "open collaboration" is embraced.

- New Models of Cooperation: If U.S. automakers can reach deeper partnerships with Chinese firms—such as the Ford-CATL battery plant model in Michigan or the Stellantis-Leapmotor alliance—they can leverage China’s efficient manufacturing processes and battery technology while combining them with their own strong local sales channels and brand influence. This would allow U.S. firms to quickly fill the gap in "cost-effective" models.

- Sharing Market Interests: Through joint investments in new factories, U.S. automakers can bypass redundant R&D costs and utilize China’s optimized supply chain—from tires and cockpits to electric motors—to lower per-vehicle costs. This not only protects domestic jobs but also ensures that U.S. firms retain a voice in the global "mass-market" segment (vehicles under $30,000).

Conclusion

"In me the tiger sniffs the rose."

Chinese automakers are like the "tiger" emerging from the cage, reshaping the rules with unstoppable competitiveness. Meanwhile, U.S. automakers must "sniff the rose"—carefully observing opportunities for cooperation while guarding against competitive pressure, searching for the beauty of co-evolution within the cracks of a changing era. Post-2026, the auto industry is no longer a simple zero-sum game, but a global symphony of efficiency, security, and survival.

Key Data Comparison (2021 vs. 2025)

- Global EV Penetration: Increased from ~8% to ~25%.

- China’s Share of Global Production/Sales: Stabilized at approximately 60%.

- Battery Costs: Decreased by about 40% over five years; Chinese LFP batteries have entered the $60/kWh era.