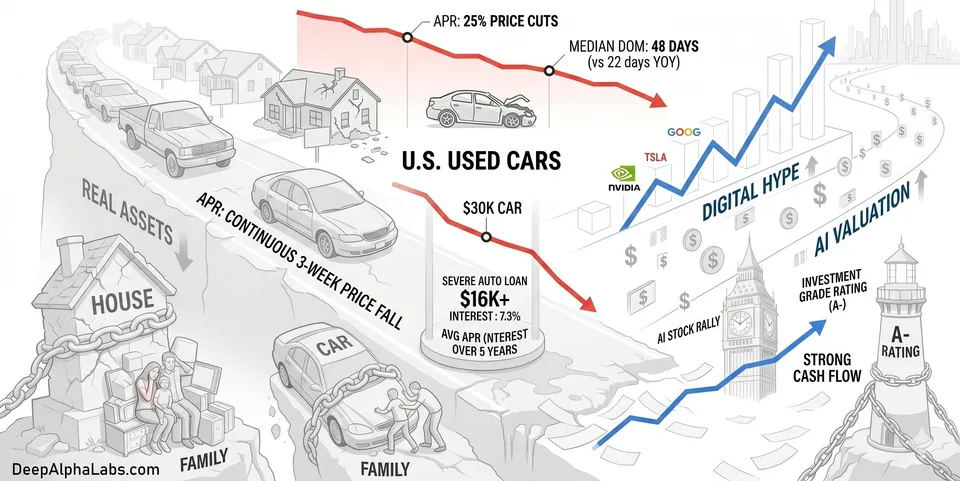

While U.S. existing homes and used cars are seeing price cuts, AI-related stocks are surging to new highs—a divergence that signals escalating systemic risk.

In April, 25% of U.S. existing home listings saw price reductions, with the median days-on-market stretching to 48 days, up from 22 days a year prior. With 30-year fixed mortgage rates hovering around 6.45%—and exceeding 7% for those with credit scores below 680—persistently high rates continue to stifle buyer appetite.

The used car market tells a similar story. Severe auto loan delinquencies (60+ days overdue) have climbed to 7.3%. In April 2026, the average APR for middle-class borrowers with average credit hit a staggering 18.5%. This means for a $30,000 vehicle, interest payments alone over five years exceed $15,000.

Real estate represents the accumulated wealth (assets) of the middle class; declining prices suggest vanishing liquidity. Automobiles represent consumer leverage (liabilities); falling prices indicate that credit expansion has hit its limit.

While AI undoubtedly represents the future and its stock rallies are not without merit, the AI narrative is ultimately anchored to the broader economy. If the macro environment crumbles, how long can AI remain a solitary oasis of growth?