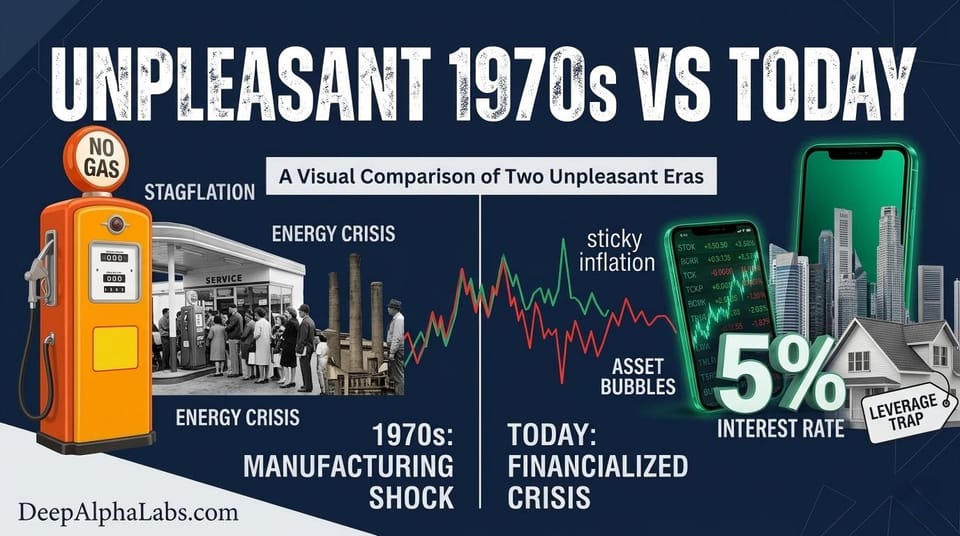

Will the "Unpleasant 1970s" Return? High Inflation, High Rates, and the New Leverage Trap

The 1970s Template: Energy Shocks and Stagflation

The 1970s were bookended by two massive oil shocks deeply tied to Iran and Middle Eastern instability. In 1973, the OPEC embargo caused oil prices to quadruple. By 1979, the Iranian Revolution triggered a second crisis, doubling prices again within a year.

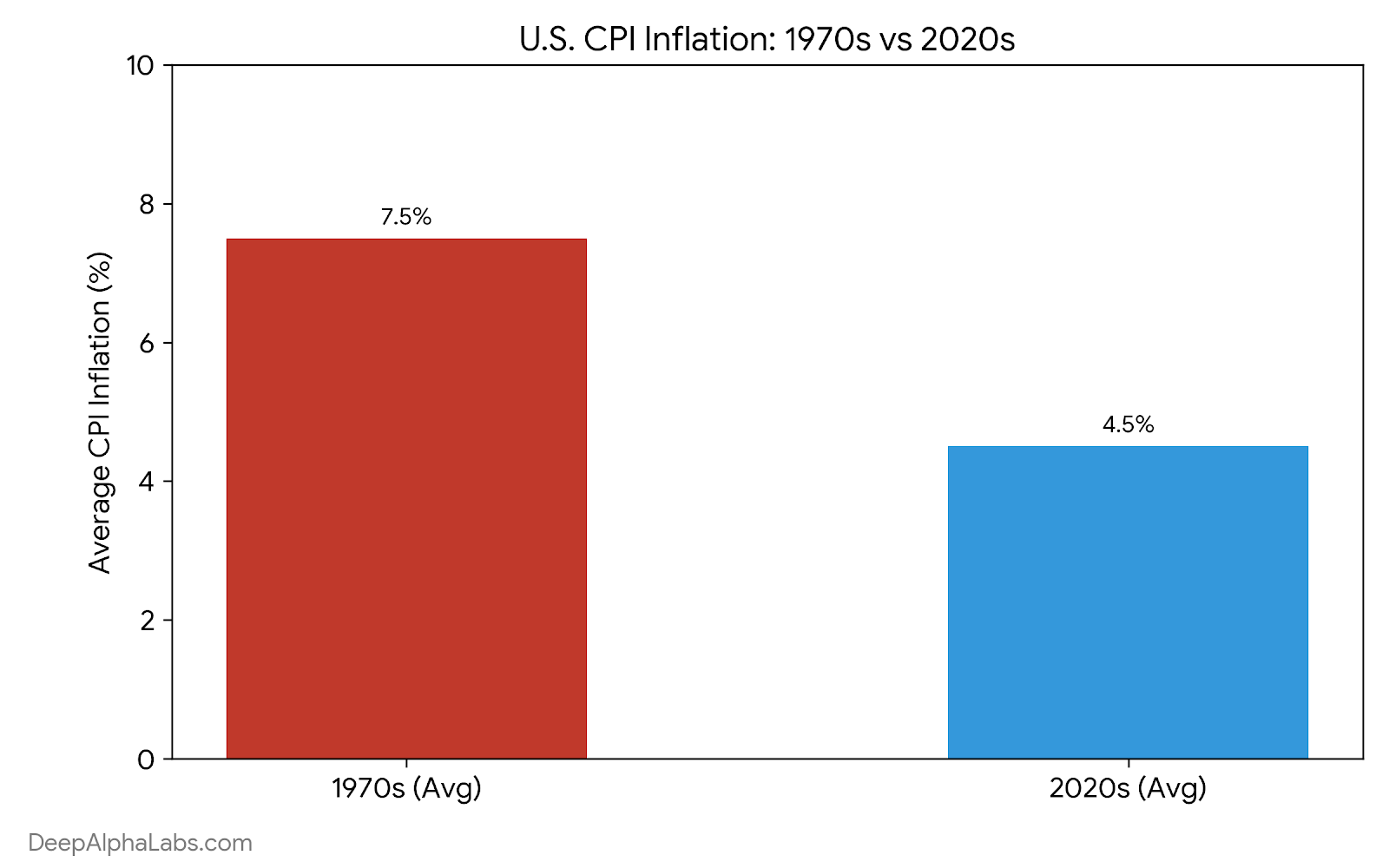

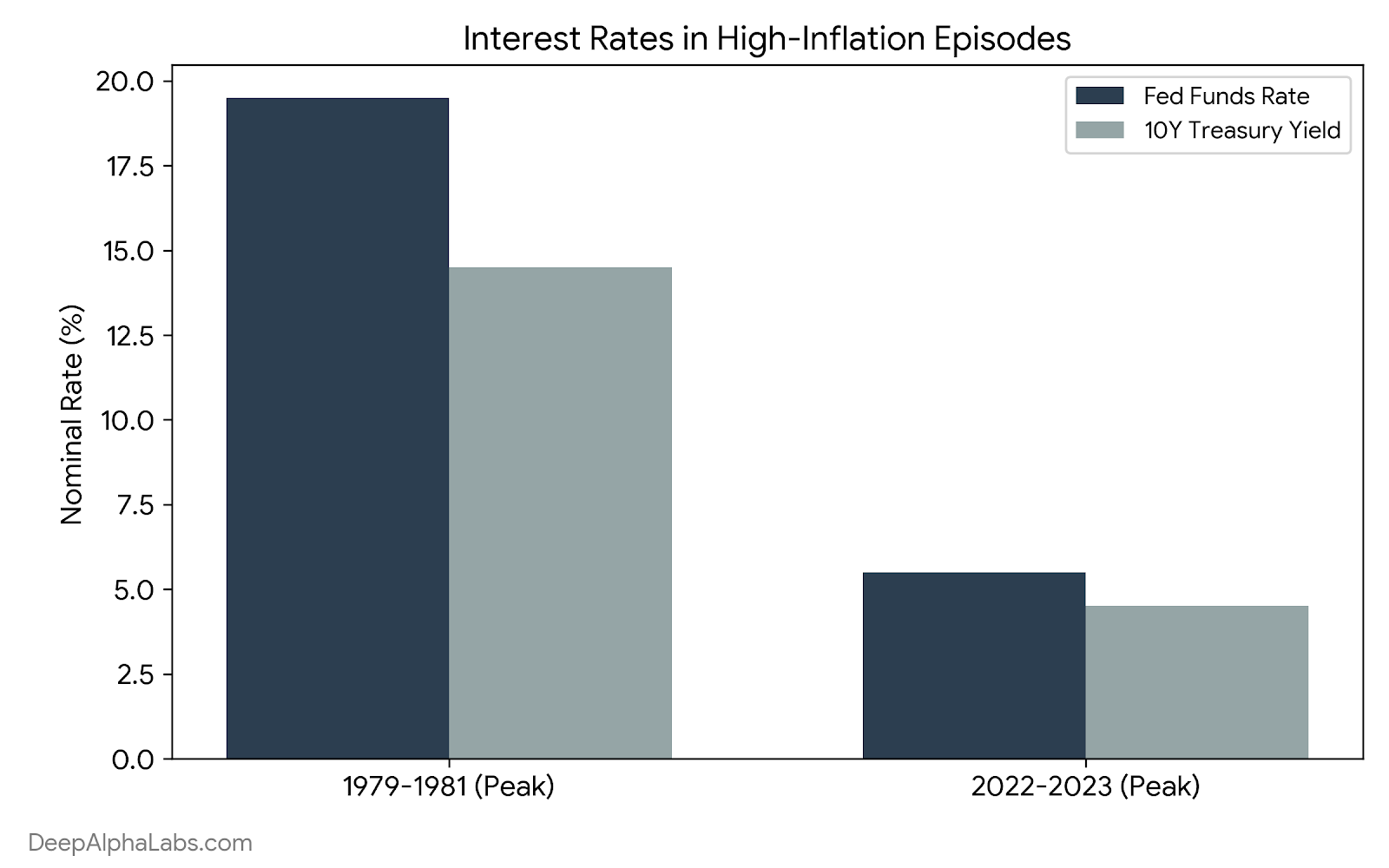

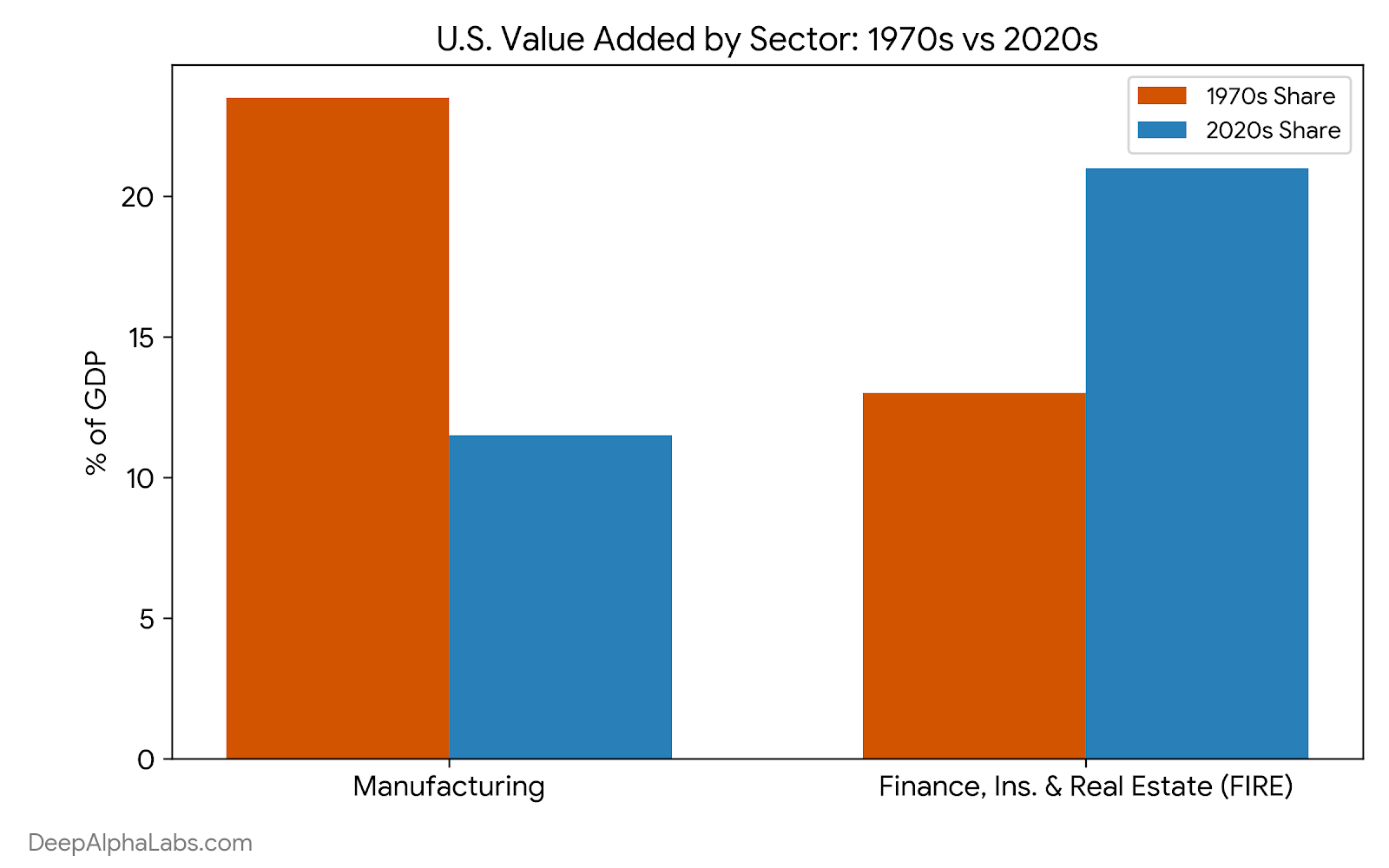

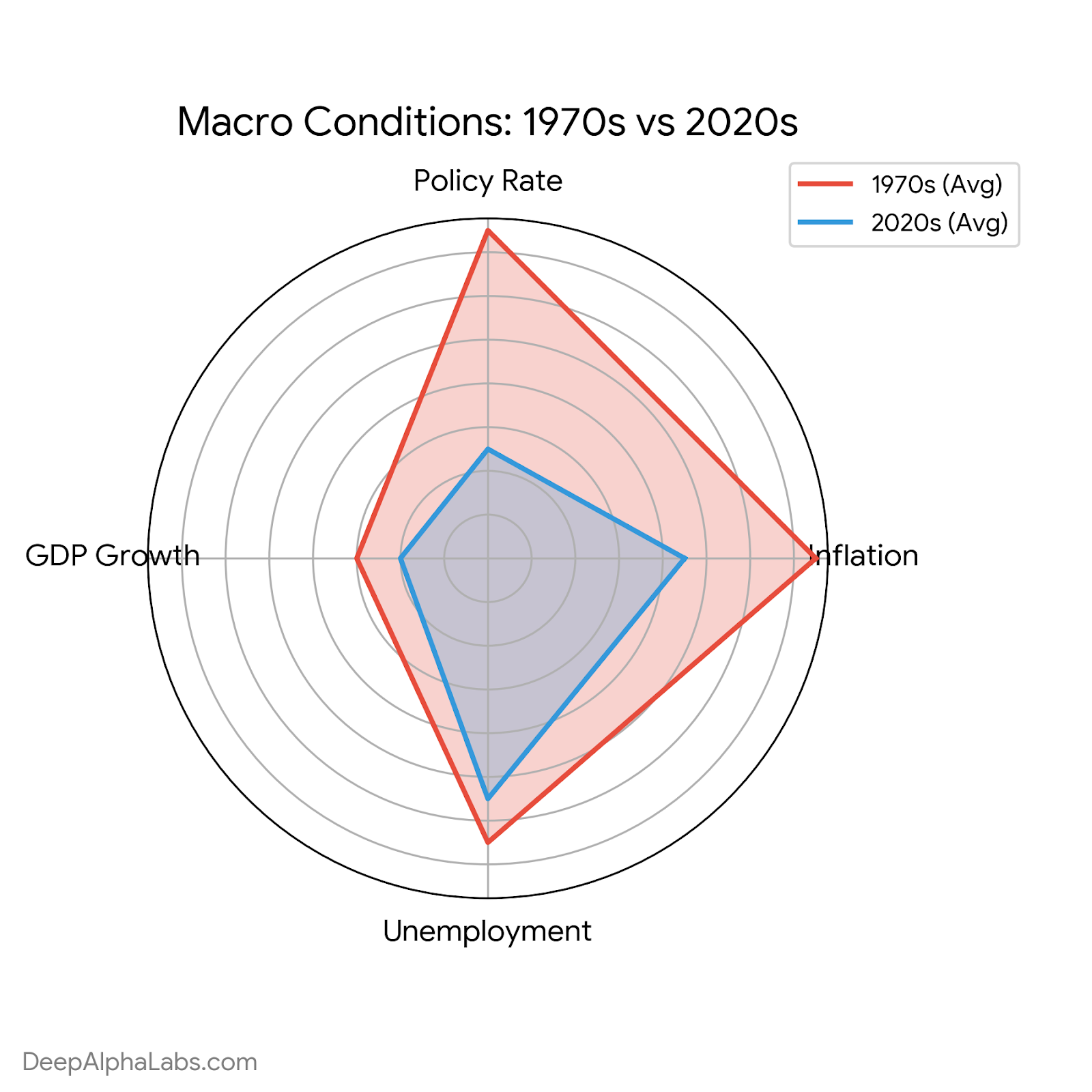

The economic fallout was devastating. By 1980, U.S. inflation (CPI) peaked at over 13%. To break this cycle, Fed Chair Paul Volcker pushed interest rates into the double digits, intentionally triggering deep recessions to kill inflation. This created "Stagflation"—a toxic mix of high unemployment and high prices. However, in the 1970s, the U.S. was still a manufacturing powerhouse. While factory workers faced layoffs, the impact was largely felt in "income"—people struggled because wages couldn't keep up with the cost of bread and gasoline.

Today’s Echoes: Iran, Oil, and Interest Rates

The current macro environment looks like a "miniature 1970s." Once again, geopolitical conflict involving Iran has pushed a massive risk premium into oil prices. This energy pressure makes the Fed’s 2% inflation target feel like a distant dream.

Like the late 70s, the Fed has been forced to keep rates "higher for longer." While today’s 4–5% rates are lower than Volcker’s 20%, they represent a violent shift from the "Zero Interest Rate Policy" (ZIRP) of the last decade. The common threads are unmistakable: geopolitical supply shocks, sticky inflation, and a central bank forced into a hawkish corner.

The Modern Twist: A Financialized Economy

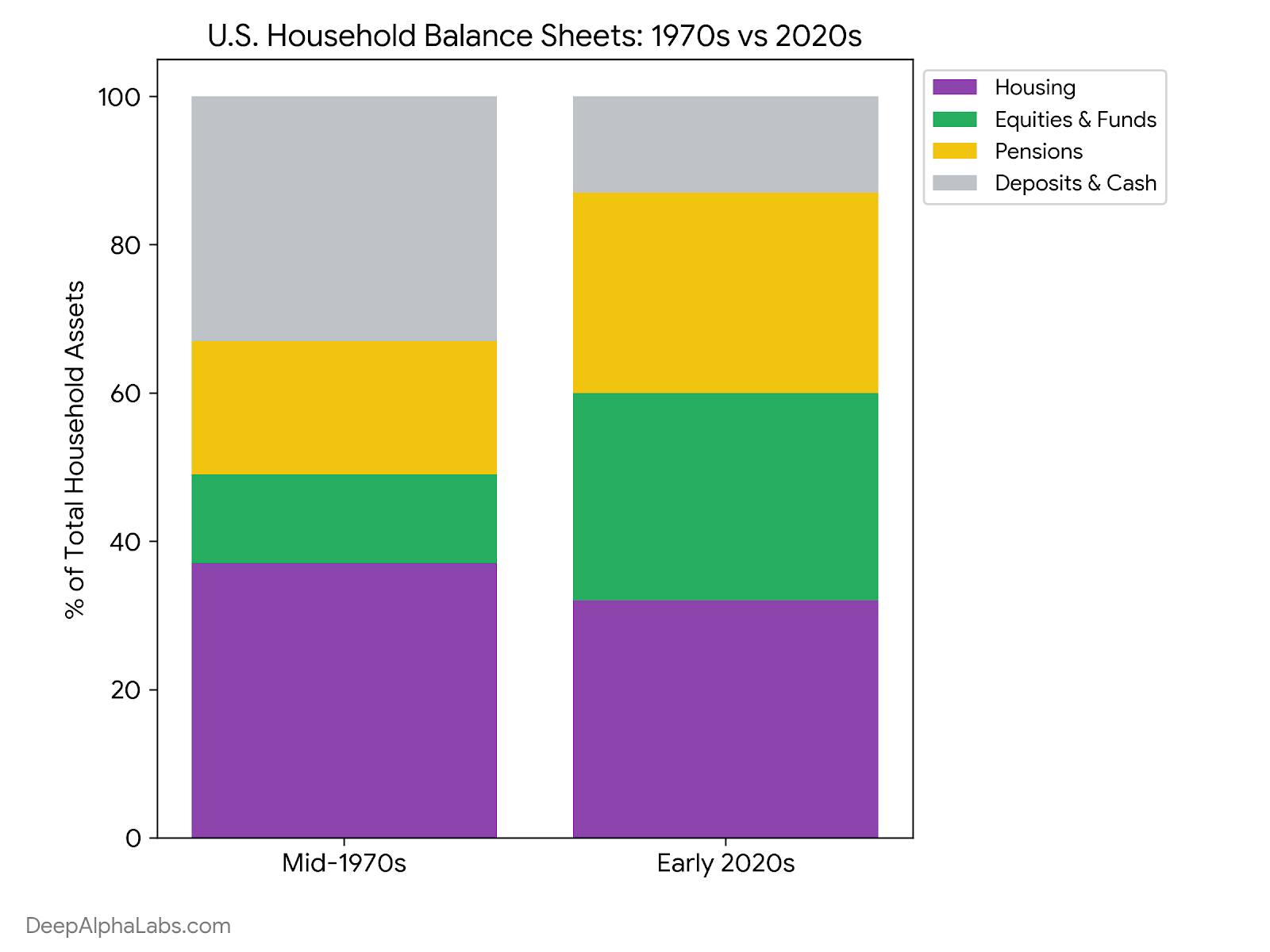

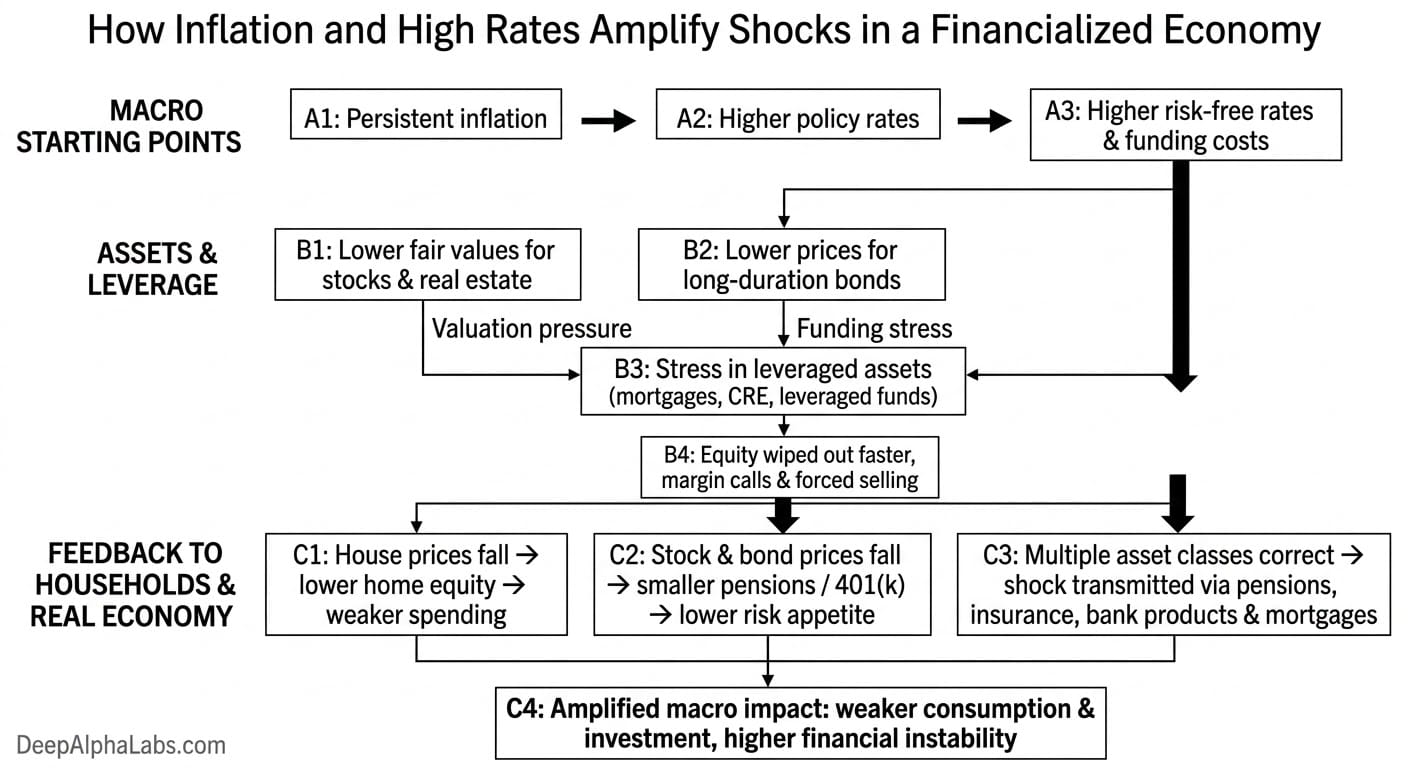

The most dangerous difference today lies in our economic structure. In 1970, the economy was driven by steel and cars; today, it is driven by Finance, Technology, and Real Estate. These sectors account for over 70% of U.S. GDP and are built on a mountain of leverage.

In the 1970s, a rate hike meant fewer new factories. Today, a rate hike attacks asset prices. Because modern wealth is tied to 401(k)s, home equity, and leveraged investment vehicles, high rates do more than just slow down spending—they threaten to wipe out the balance sheets of the middle class.

When inflation stays high and rates rise:

- Valuations Collapse: Higher "risk-free" rates automatically lower the fair value of stocks and long-term bonds.

- The Leverage Multiplier: In a world of mortgages, commercial real estate loans, and leveraged ETFs, a small dip in asset prices can trigger margin calls and forced selling, amplifying the downward spiral.

- Widespread Impact: In 1970, few people held complex financial portfolios. Today, if the stock and bond markets shake simultaneously, it immediately hits pensions, insurance products, and household savings.

Conclusion: Same Spark, Bigger Fuse

While the U.S. is more energy-independent today than in 1973, our economy is far more sensitive to interest rate shocks due to extreme financialization. The 1970s were a crisis of income and production; the 2020s are shaping up to be a crisis of assets and leverage.

The "unpleasantness" of the 70s was felt at the gas pump and in the unemployment line. Today, the same geopolitical sparks could ignite a fire that burns through the very foundation of modern wealth—our homes and our retirement accounts. We may not see 13% inflation, but in a world of high debt, even 4% inflation and 5% rates can be just as painful.

History doesn’t repeat itself, but it often rhymes. As we navigate 2026, the ghost of the 1970s—a decade defined by "Stagflation"—is haunting global markets. Back then, the combination of high inflation, soaring interest rates, and stagnant growth created an "unpleasant decade" that eroded wealth and crushed the American dream. Today, with Middle East tensions rising and inflation proving sticky, many ask: are we reliving the 1970s, or is the modern structure of our economy making the potential shock even worse?