Japan’s Macro Risks: Soaring Debt, Stagnant Growth, an Aging Society, and a Squeezed Auto Industry

Japan faces a complex macro risk profile defined by extreme public debt, chronic low growth, rapid population aging, and structural pressure on its core automotive industry.

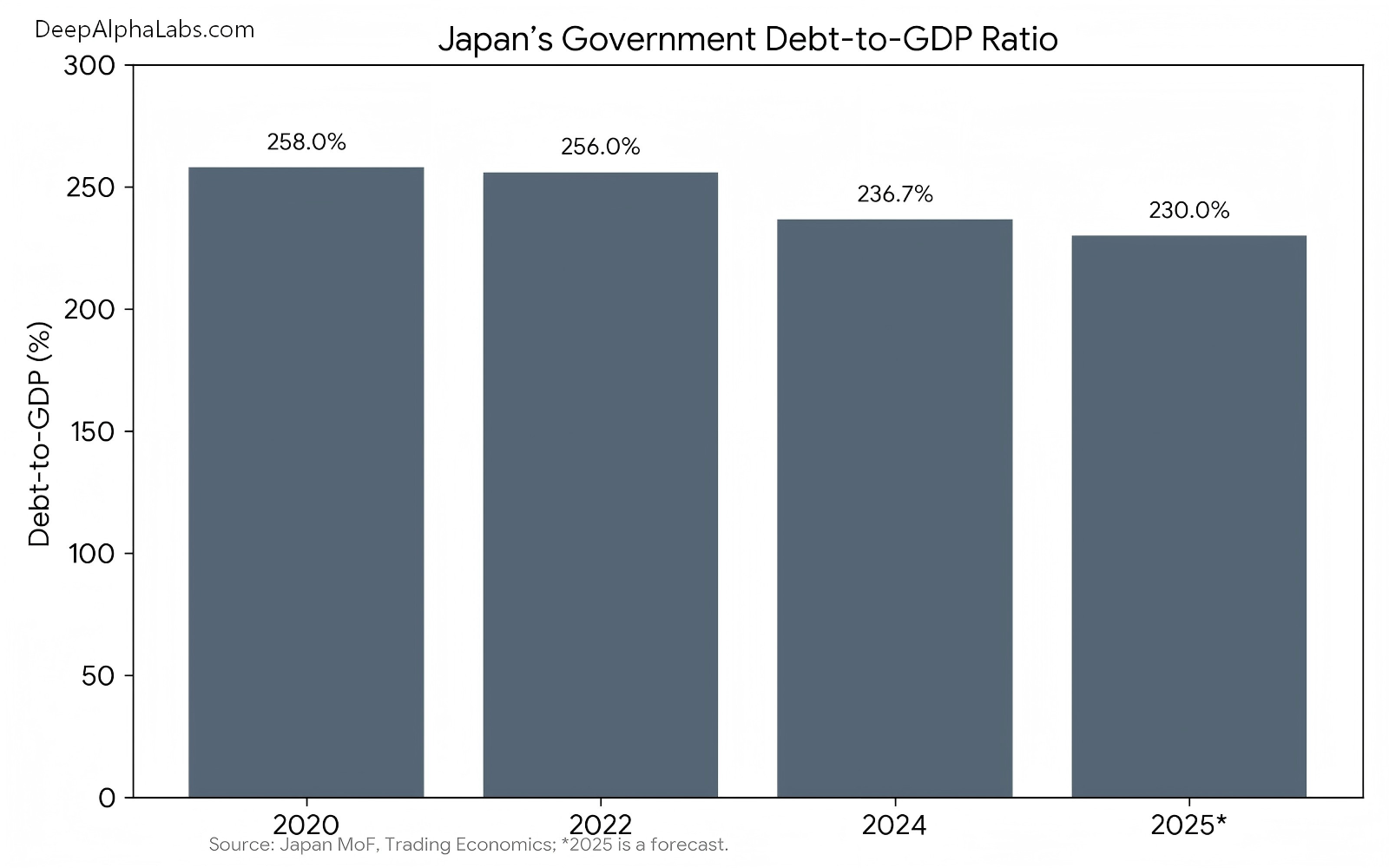

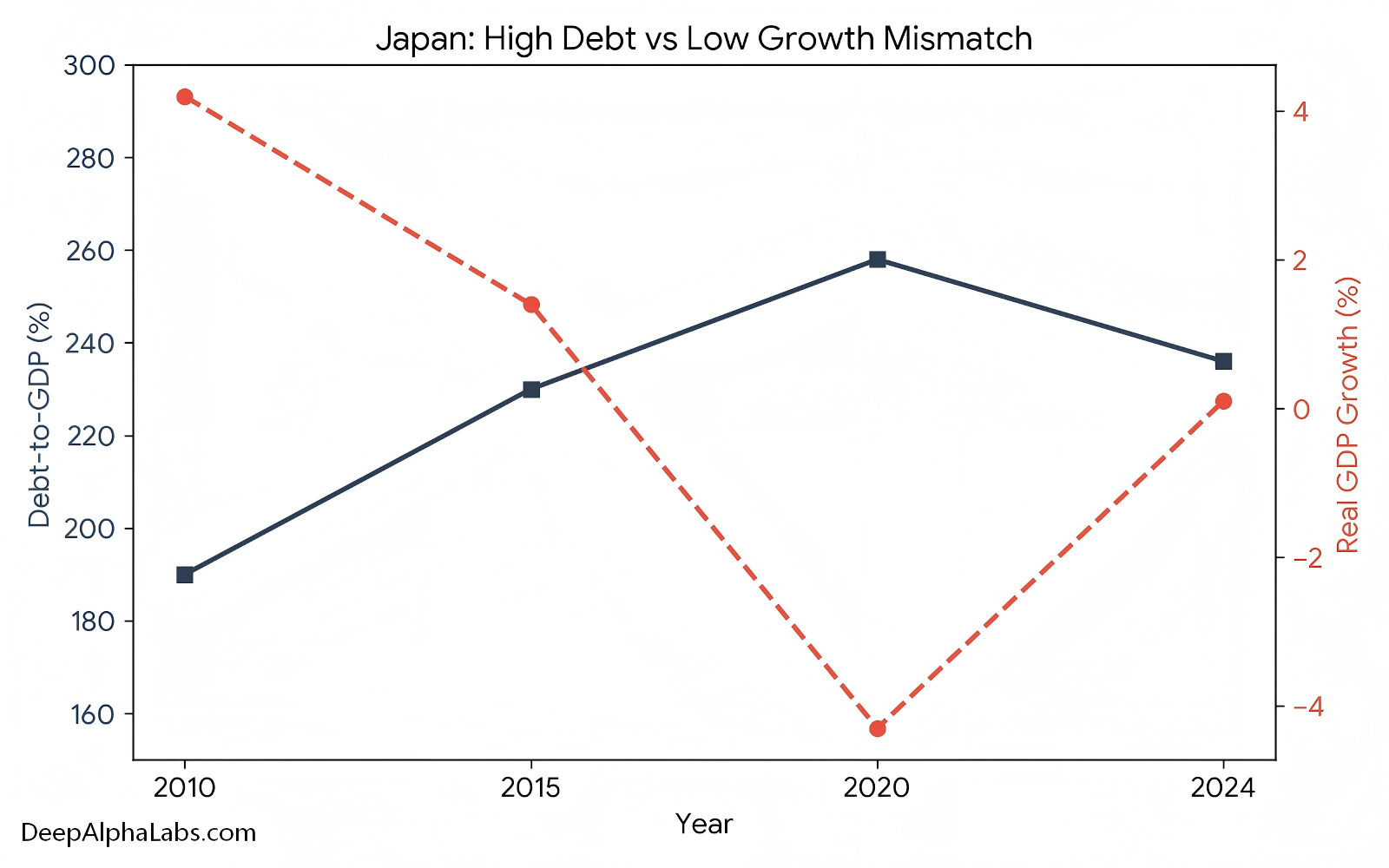

Japan’s public finances are the most stretched among major economies. General government gross debt stood at about 236.7% of GDP in 2024, down slightly from a pandemic peak of 258.4% in 2020, but still by far the highest ratio in the world. In nominal terms, Japan’s debt is estimated at roughly 13.3 trillion USD against a GDP of about 6.4 trillion USD at the end of 2025. This debt burden has been sustainable primarily because interest rates have been extraordinarily low and the bulk of government bonds are held domestically by the Bank of Japan, banks, insurers, and pension funds. However, as the Bank of Japan cautiously normalizes policy and 10‑year JGB yields drift toward 1%, the long‑run interest bill on such a large stock of debt will gradually rise, increasing fiscal vulnerability.

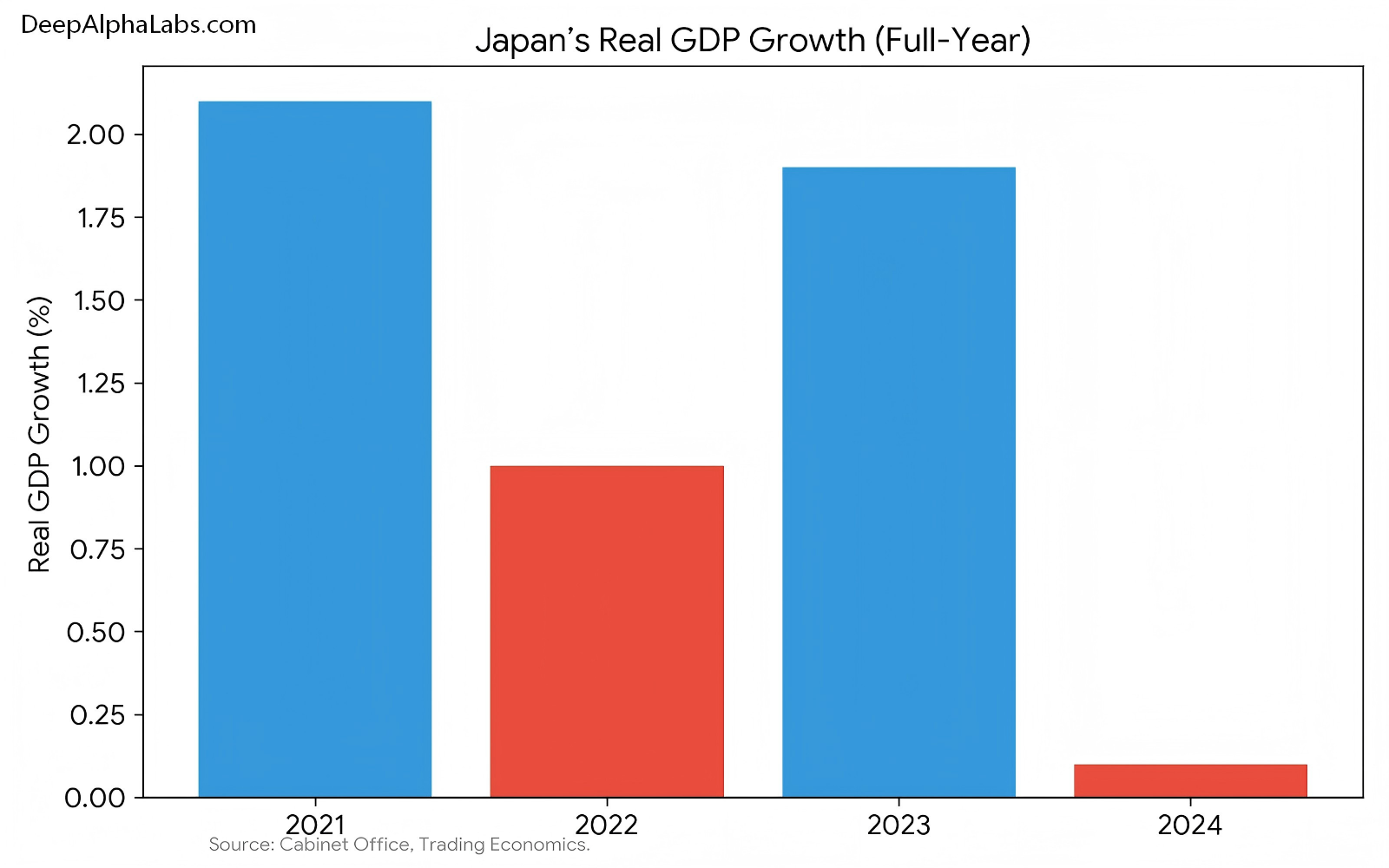

On the growth side, Japan has effectively been in a low‑growth regime for decades. Full‑year GDP growth slowed to just 0.1% in 2024, down from 1.9% in 2023, marking the weakest performance since 2020. Trading Economics’ consensus expects growth to remain around 0.5% in 2025 and only 0.7% in 2026, underscoring how limited Japan’s potential growth has become. Private consumption, which accounts for more than half of GDP, actually declined 0.1% in 2024 as real wages lagged behind inflation, highlighting the squeeze on household purchasing power. Investment has been volatile, often supported more by fiscal stimulus and weak yen–driven export competitiveness than by robust domestic demand.

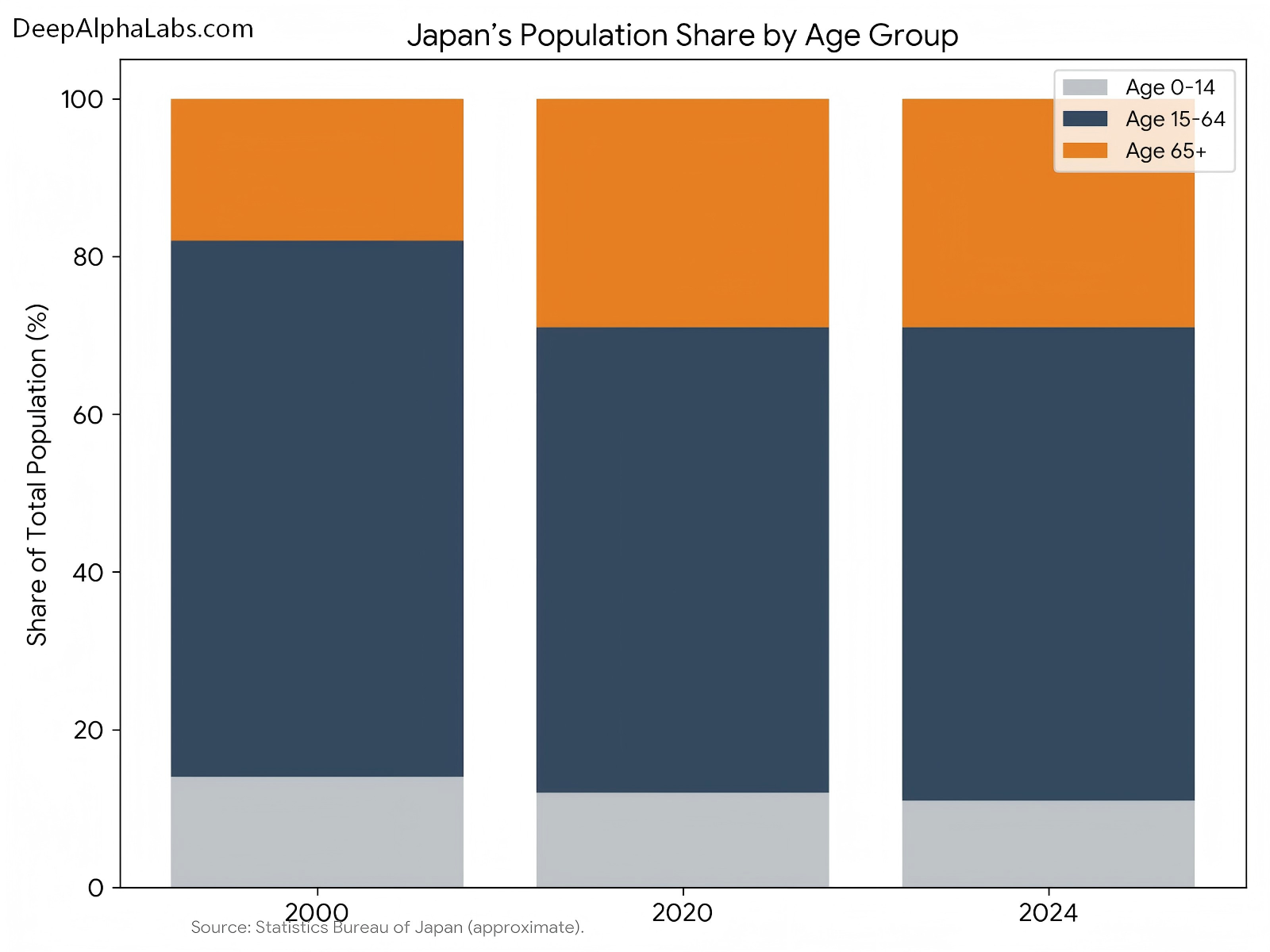

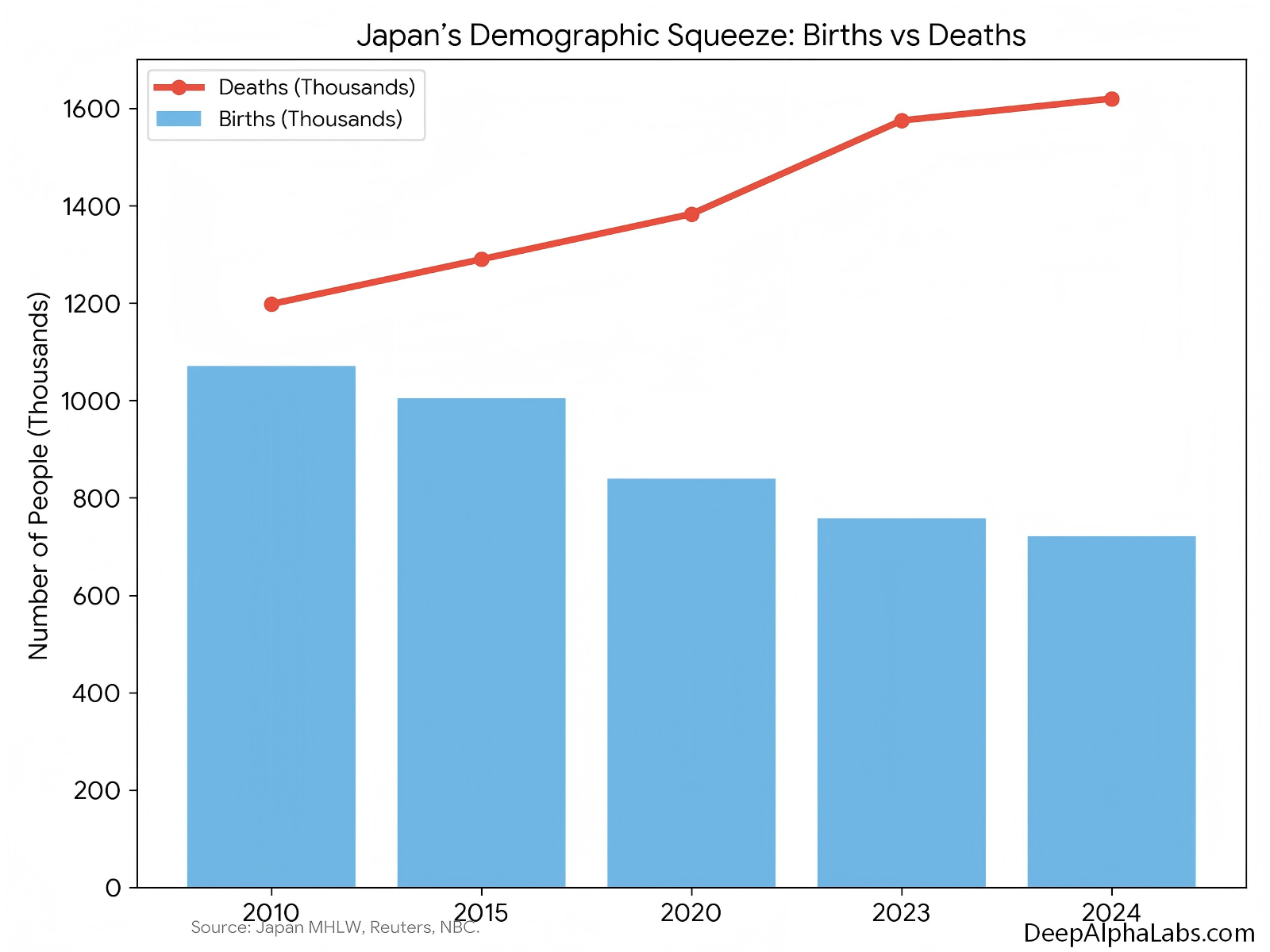

Demographics amplify these structural headwinds. Japan recorded only 720,988 births in 2024, the ninth consecutive annual decline and the lowest figure since records began in 1899. Births fell about 5% from the previous year, while deaths reached roughly 1.62 million, meaning more than two people died for every newborn. The total fertility rate is estimated around 1.2, far below the replacement level of 2.1. As a result, the population is shrinking and aging rapidly: people aged 65 and over already account for close to 30% of the population, one of the highest old‑age shares globally. This demographic profile erodes the labor force, depresses domestic demand, and increases pressure on pension and healthcare systems, all while the tax base is shrinking.

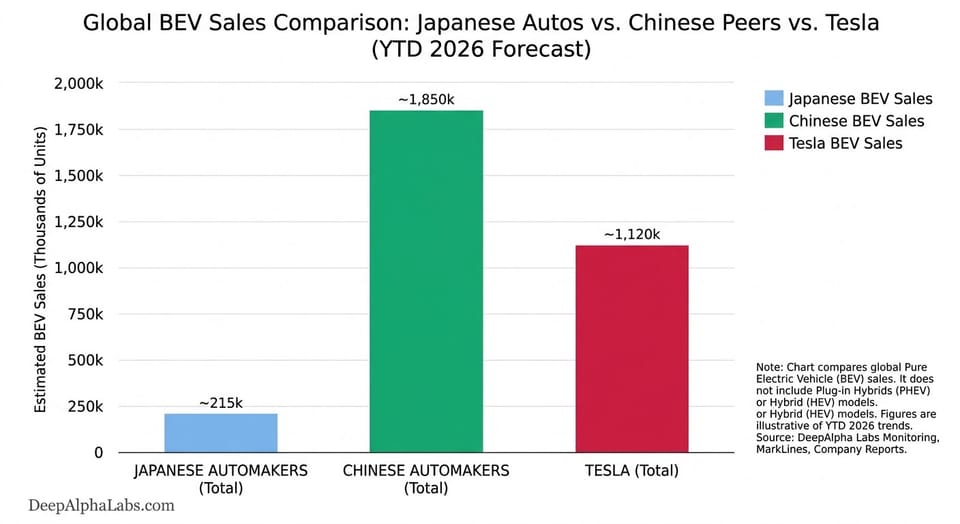

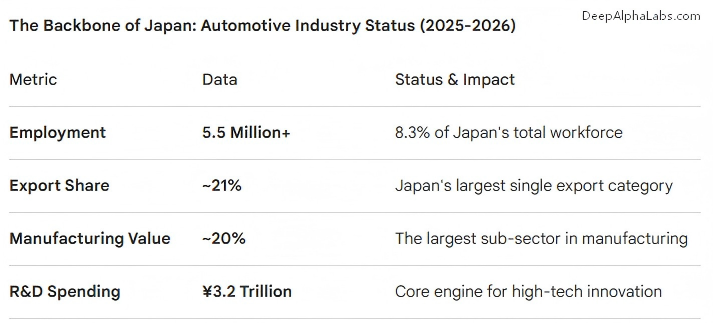

Within this macro context, the automotive industry is a critical but vulnerable pillar. According to the Japan Automobile Manufacturers Association and Toyota data, auto manufacturing and auto‑related industries directly and indirectly employ around 5.5 million people, roughly 8–10% of Japan’s total workforce, and account for about 10–20% of exports and foreign‑currency earnings. This makes autos arguably Japan’s last truly global-scale, mass‑employment manufacturing stronghold, after consumer electronics and home appliances ceded global leadership to competitors in Korea and China. Yet the global shift toward battery electric vehicles and software‑defined cars poses a structural challenge to Japan’s traditional strengths in internal combustion engines, hybrids, and incremental quality improvement.

If Japanese automakers were to lose significant global share or profitability during the EV and autonomous transition, the macro impact would be substantial.

A 20–30% contraction in auto‑related output and employment over the next decade would not only directly hit GDP and exports but also indirectly weaken tax revenues and high‑quality manufacturing jobs in a country already grappling with high debt and severe aging. Japan would likely avoid a sudden crisis thanks to its high domestic savings and large net foreign asset position, but could drift further into a path of “slow shrinkage”—low or negative real growth, rising fiscal sustainability concerns, and a gradual decline in its relative weight in the global economy.