Vertical Integration vs. Fragmented Supply Chains in the EV Sector ( US vs. China Economy Part 2 )

Executive Summary

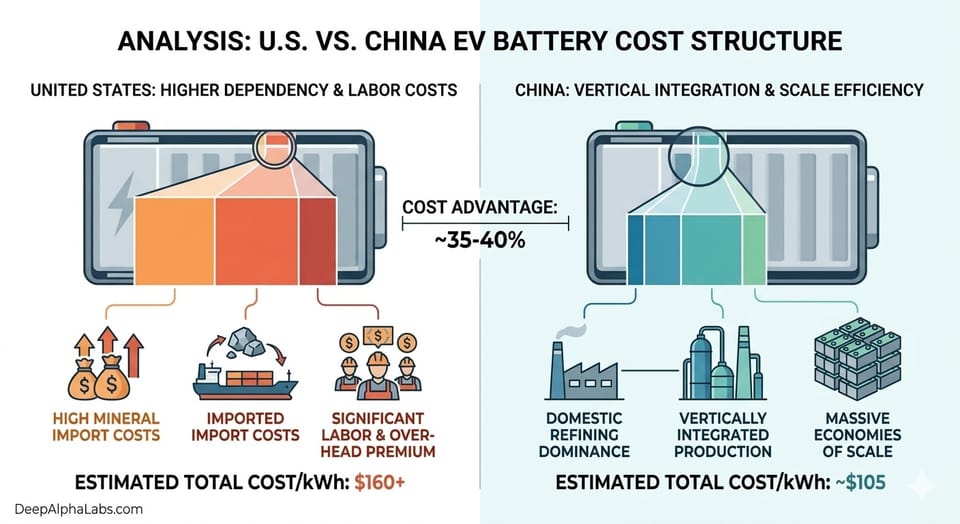

The global transition to electromobility has shifted the competitive landscape from internal combustion engine (ICE) efficiency to upstream supply chain dominance. This analysis deconstructs the structural advantages that allow Chinese Original Equipment Manufacturers (OEMs) to maintain a significant cost lead over their American counterparts.

1. Upstream Critical Mineral Refining

The "de-risking" of the EV supply chain remains a primary hurdle for the United States. While mineral extraction is global, midstream chemical processing is concentrated in China.

- Market Share: China manages approximately 80% of global cobalt refining and dominates the anode market via its control over graphite processing.

- Strategic Bottleneck: US domestic production is hampered by prolonged permitting cycles, making it difficult to meet the "Domestic Content" requirements of the Inflation Reduction Act (IRA) without increasing final MSRP.

2. Battery Cell Manufacturing and Chemistry Trends

Battery energy density and cost-per-kilowatt-hour ($/kWh) are the primary metrics of EV competitiveness.

- LFP Dominance: China leads in Lithium Iron Phosphate (LFP) technology. LFP batteries are cobalt-free, safer, and significantly cheaper to produce.

- Economies of Scale: With over 3,000 GWh of planned capacity, China benefits from a "vertical integration" model. Companies like BYD produce their own cells, semiconductors, and motors, reducing the "middleman" markup prevalent in the US Tier-1 supplier model.

3. Regionalized Clusters and Speed-to-Market

China’s "3-hour Supply Chain Circle" in the Yangtze River Delta provides a logistical advantage that the US "Rust Belt" currently lacks.

- Agility: The average development cycle for a Chinese EV is 30% to 50% faster than the global industry average.

- Capex Efficiency: Lower capital expenditure requirements and high automation levels allow Chinese manufacturers to price vehicles like the BYD Seagull at levels currently unattainable for US manufacturers.

Strategic Outlook

The US competitive advantage remains concentrated in Full Self-Driving (FSD) software and silicon architecture. However, without a localized midstream supply chain for cells and minerals, American OEMs face a persistent 30%+ cost disadvantage. The next decade will determine if US protectionist policies (tariffs and subsidies) can successfully bridge this industrial gap.